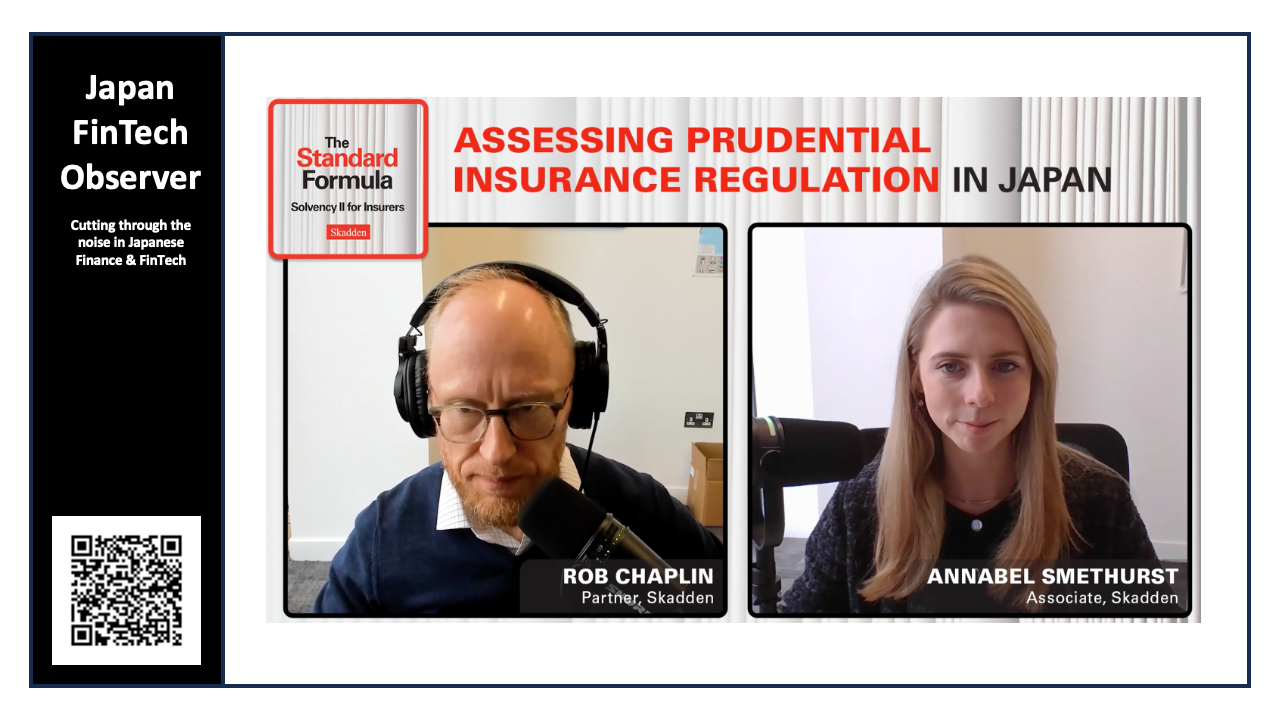

Skadden: Assessing Prudential Insurance Regulation in Japan

This "Standard Formula" podcast episode by Skadden delves into the intricate landscape of prudential insurance regulation in Japan, a topic gaining traction due to its significant impact on the burgeoning reinsurance market. As part of a year-long series exploring global solvency requirements, the discussion is anchored by Japan's position as the fourth-largest insurance market worldwide, holding a 5% global share and generating premiums of $363 billion in 2024. Historically dominated by life insurance, Japan's market is witnessing increased competition with the influx of foreign insurers, further fueled by ongoing regulatory reforms aimed at bolstering financial stability and aligning with international standards like Solvency II and the IAIS Insurance Capital Standard (ICS).

Japan's regulatory journey has seen a shift from rigid, formal solvency rules to a more dynamic, risk-based approach, initiated by the "Financial Big Bang" in the 1990s. This liberalization encouraged greater openness and flexibility, allowing insurers to compete on price and service, and facilitated the entry of foreign players. The Insurance Business Act of 1995 epitomized this spirit, prompting mass consolidation and restructuring, and enabling non-life insurers to access the life insurance market through subsidiaries. The result has been a substantial increase in foreign investment, with foreign insurers now holding significant market shares in both life and non-life sectors.

Deregulation has also spurred changes in reinsurance purchasing. Historically, the market retained reinsurance internally through pooling arrangements, but liberalization and the impact of natural disasters led to insurers seeking their own reinsurance facilities. This trend is accelerating, establishing Japan as a reinsurance hub. The appeal for foreign reinsurers lies in the mature and competitive market, coupled with a growing demand for savings-oriented products and morbidity coverage driven by an aging population and limitations in public healthcare. This necessitates sophisticated underwriting, balance sheet relief, and asset management partnerships, all achievable through reinsurance.

Reinsurance transactions typically involve sessions from onshore Japanese insurers to offshore reinsurers, particularly those based in Bermuda, a jurisdiction favored due to the FSA's comfort with its regulatory equivalence. These transactions often aim to provide capital relief and are structured as both in-force and flow arrangements. A notable characteristic is the prevalence of reinsurers affiliated with large asset managers, reflecting Japanese insurers' desire for investment management support.

The regulatory framework is overseen by the Financial Services Agency (FSA), which is responsible for ensuring the stability of Japan's financial system. While Japan has been deemed Solvency II equivalent, it is now moving towards implementing economic value-based solvency regulations closely aligned with the ICS. This entails adapting the ICS to the unique characteristics of Japanese insurers, particularly the prevalence of small and medium-sized entities.

Despite ongoing alignment with international standards, certain nuances exist. For instance, fronting is neither explicitly prohibited nor permitted. Exceptions to licensing requirements are granted for certain reinsurance contracts and cases where the FSA provides advanced permission for purchasing insurance from unlicensed foreign companies. There is also increased FSA scrutiny of reinsurance practices, particularly concerning transactions with reinsurers backed by private equity, potentially leading to new regulatory measures. Historically, Japanese insurers have also utilized the UK's Part 7 transfer mechanism for legacy businesses and have established insurance broking subsidiaries in the UK. Overall, Japan's evolving insurance landscape reflects a balance between policyholder protection, regulatory equivalence, and the need for competitive innovation, both for domestic and international players.

On a similar topic, you might be interested in our podcast with Dr. Sahin, discussing the Japanese insurance law & history, accounting for both a historical perspective and taking a current snapshot.

Please follow us to read more about Finance & FinTech in Japan, like hundreds of readers do every day. We invite you to also register for our short weekly digest, the “Japan FinTech Observer”, on LinkedIn, or directly here on the platform.

We also provide a daily short-form Japan FinTech Observer news podcast, available via its Podcast Page. Our global Finance & FinTech Podcast, “eXponential Finance” is available through its own LinkedIn newsletter, or via its Podcast Page.

Should you live in Tokyo, or just pass through, please also join our meetup. In any case, our YouTube channel and LinkedIn page are there for you as well.