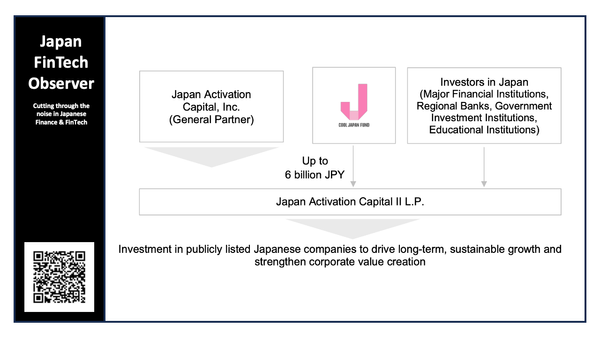

Legal system for digital money

The Bank of Japan's Institute for Monetary and Economic Studies (IMES) is conducting research on legal systems with a focus on digital money. In a newsletter published last week in Japanese, they have introduced some of their latest research findings.

- What is Digital Money

- Research Introduction

- Transactions Using Digital Money

- New Concepts Regarding Electronic Data

- Handling of Information

- Conclusion

1. What is Digital Money

In our daily consumption activities, we use various payment methods.

Payment methods include cash, gift certificates, bank transfers using deposit accounts, as well as those based on information and communication technology such as prepaid cards, credit cards, debit cards, and IC cards. Recently, the use of QR code payments has expanded. Cryptocurrencies and stablecoins have also become topics of discussion.

Digital money is a general term referring to payment methods based on digital technology. Therefore, excluding cash and gift certificates, there is no clear consensus on which payment methods qualify as digital money.

The term "digital money" has come into use relatively recently. It began appearing in legal journals from the latter half of the 2010s. Looking at its usage in legal literature, digital money appears to encompass cryptocurrencies, stablecoins, and broadly, smartphone-based payment methods.

A similar term to digital money is electronic money. The term electronic money spread with the emergence of prepaid IC cards around 2000 and is commonly used to refer to contactless payments. In recent years, the spread of distributed ledger technology and QR codes has led to an awareness of differences from electronic money, which may be one reason why the term digital money has come into use. In any case, it is important to clarify the definitions of electronic money and digital money when discussing these topics (incidentally, "cashless" is a convenient term that encompasses both).

From a legal perspective, one approach is to define digital money as payment methods regulated under the Payment Services Act that are based on digital technology. The Payment Services Act was established in 2009 (enforced the following year) in response to the rapid spread of transportation IC cards, among other factors. It has since been amended to address various situations such as the bankruptcy of virtual currency exchanges, the expansion of fund transfers, and the emergence of stablecoins. Currently, the main regulated payment methods are prepaid payment instruments, fund transfers, electronic payment methods, and crypto assets.

2. Research Introduction

Digital money is institutionally provided for by the Payment Services Act, but as a relatively new payment method, it is important to accumulate legal discussions similar to those established for cash and bank transfers. Considering the increasing importance of digital money as a payment method in Japan, the Institute for Monetary and Economic Studies has been conducting research on legal issues related to digital money.

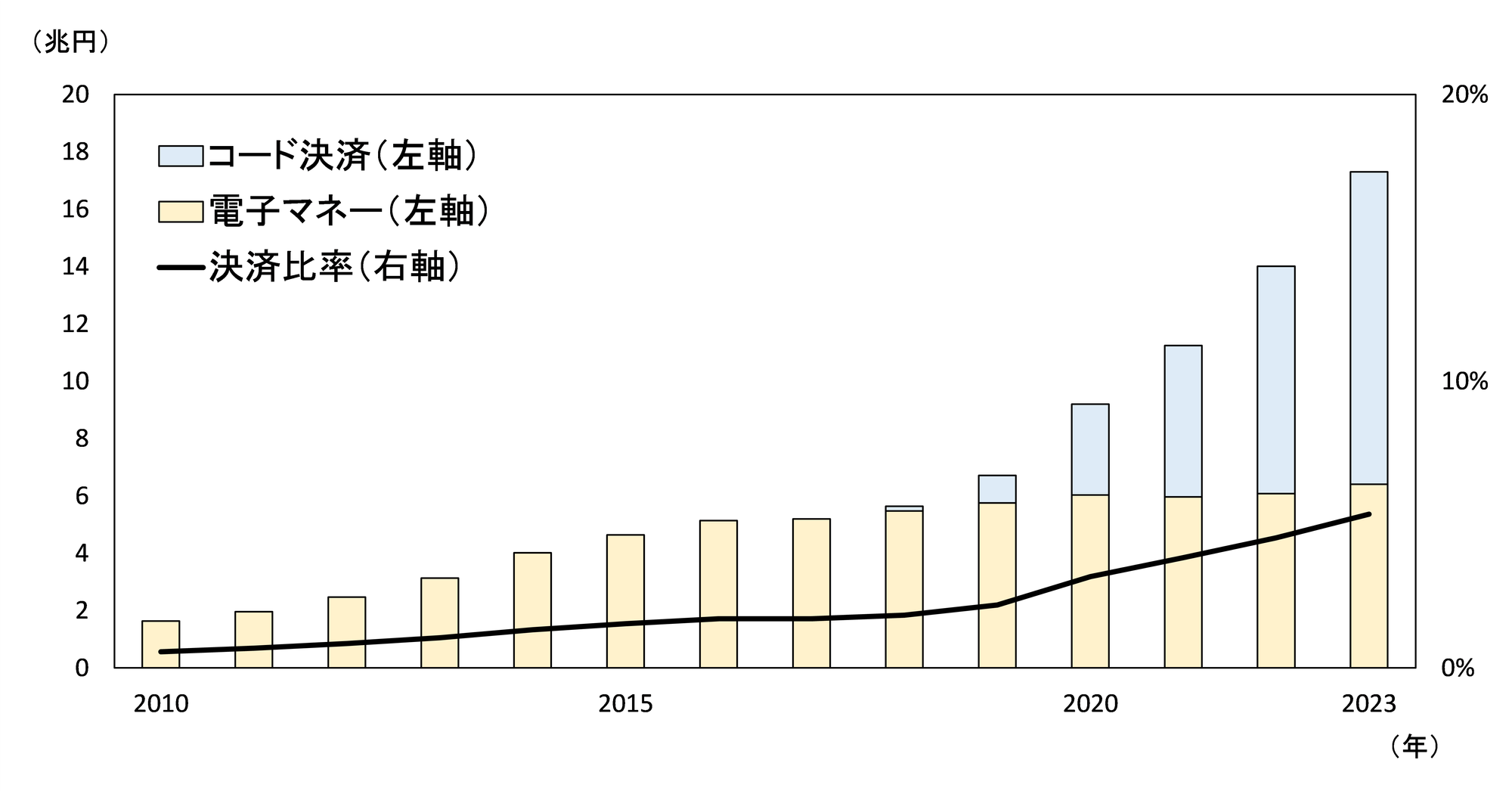

QR Code Payments and Electronic Money Payment Amounts and Settlement Ratio

The figures from METI's "Calculation of Cashless Payment Ratio for 2023" are as follows:

- QR code payment amount (blue) is the "store usage amount" from the Cashless Promotion Council's "QR Code Payment Usage Trend Survey" minus "credit card usage," (aggregated from data provided by QR code payment providers who cooperated with the survey)

- Electronic money payment amount (yellow) is from the Bank of Japan's "Payment Trends," "Electronic Money" settlement amount (targeting IC-type electronic money of the prepaid method, aggregated from data provided by surveyed businesses)

- The settlement ratio in the graph (line) is calculated by dividing the sum of QR code payments and electronic money payments by private final consumption expenditure, following METI's definition of cashless payment ratio

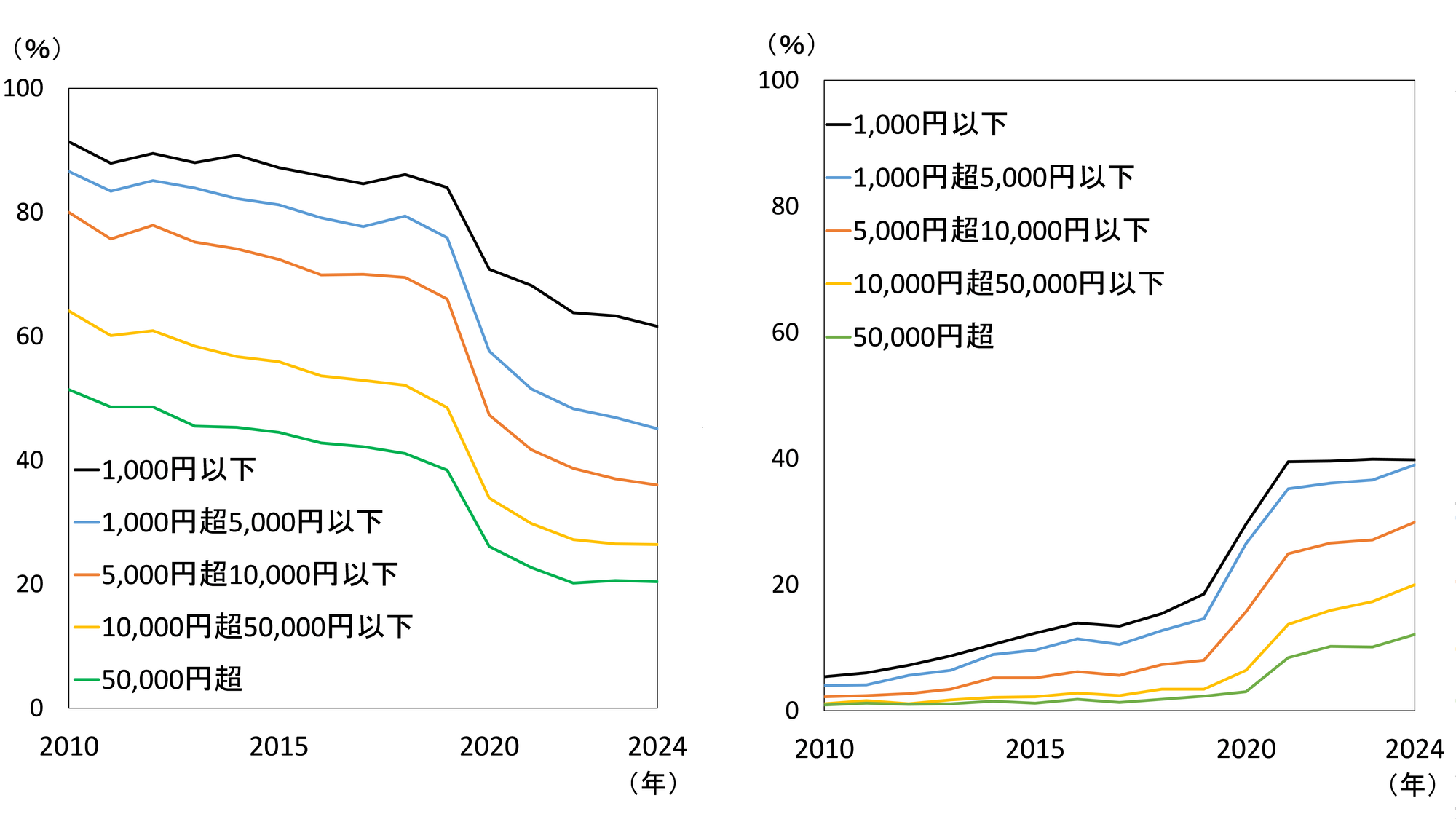

Daily Payment Methods

Percentage of people who frequently use cash (graph on the left), and percentage of people who frequently use electronic money (graph on the right.

The graphs shows the percentage of respondents who answered the question "How does your household use different payment methods for daily payments (shopping, etc.) depending on the amount? Please select the payment methods you frequently use for each amount. (Up to 2 choices)" The answer choices were "Cash (bills and coins)," "Credit Card," "Electronic Money (including Debit Card)," and "Other."

2.a Transactions Using Digital Money

As a starting point for examining legal issues related to digital money, it is important to clarify the fundamentals of what rights we (users of digital money) have against the issuers of digital money and what legal mechanisms are used to transfer digital money to payees.

The Legal Issues Research Group report "Rights and Transfers of Digital Money" addresses this challenge. The report examines the content of rights that users have against digital money issuers and the legal structure of rights transfers, comparing with bank deposits where the legal structure is relatively established. It points out that even digital money that can be used with a sense similar to deposits may not necessarily be treated the same as deposits under the law, and the legal structure of rights and transfers may differ depending on the type.

This research group also identified various issues for consideration regarding digital money. One research that deepened the analysis of these issues is "Organization of Legal Relationships When Purchasing (Charging) Prepaid Payment Instruments with Credit Cards." This paper examines cases where users charge QR code payments with credit cards to use digital money.

When charging with cash, the cash is no longer the user's property at that point. In contrast, when charging with a credit card, the amount is not withdrawn from the user's bank account until about a month later, which can result in "post-payment" after using the digital money. Here, assuming a case where the digital money issuer fails and it becomes difficult to use the digital money, users would be motivated to stop the withdrawal of the credit card charge. This paper examines the legal relationships in such cases from a consumer protection perspective.

"Legal Examination of Loss Allocation for Fraudulent Acquisition of Digital Money: Focusing on Digital Money Provided by Fund Transfer Service Providers" is another paper that deepens the analysis of issues identified by the above research group. If digital money is fraudulently used through impersonation, there is a question of whether the original user or the issuer should bear the damage (while the impersonator should ultimately be responsible, they may not always be identifiable). This paper points out that deposits and digital money are subject to different rules for unauthorized withdrawals, and even within digital money, different rules may apply depending on the usage scenario. Based on this, the paper analyzes appropriate loss allocation by referring to overseas legal systems.

2.b New Concepts Regarding Electronic Data

In recent years, major legal jurisdictions abroad have shown a tendency to consider electronic data as being possessed or owned like physical items if certain conditions are met. There, the concept of "control" plays an important role and is a requirement for acquiring electronic data. In Japan as well, the concept of "control" has been discussed in relation to the digitization of bills of lading, reflecting the influence of international discussions.

While there are various types of digital money, these new concepts may be useful for considering digital money in Japan. "Basic Perspectives on 'Control' of Digital Assets" is a paper that analyzes this concept of "control" through comparison of legislation and discussions in the United States, the United Kingdom, and other countries. This paper presents basic perspectives for considering rights related to electronic data in a digital society.

"Legal Form and Transfer of Electronic Payment Methods" also focuses on the concept of "control." This paper examines the legal structure related to the transfer of electronic payment methods (so-called stablecoins) through comparison with bank transfers and overseas rules. It suggests that it would be desirable to develop civil law regulations centered on the concept of "control" in the future.

3.c Handling of Information

The handling of information generated through the use of digital money is also an important legal issue. While cash has anonymity and records of who used how much where and when are not easily kept, digital money has transaction histories that can be tracked by issuers. Although credit cards similarly leave records, digital money commonly used recently (prepaid payment instruments and fund transfers) tends to allow more information to accumulate with the issuer.

Such accumulated information can be used for proposing products that meet consumer needs and analyzing consumption trends, but it may also create tension with privacy concerns, making it important to explore appropriate methods of use. The Legal Issues Research Group report "Use of Accumulated Information and Legal Challenges" organizes legal issues regarding the handling of payment information by digital money issuers in three scenarios: the use of user information (especially profiling), the use of merchant information, and information sharing.

3. Conclusion

While the Institute for Monetary and Economic Studies has conducted research on various legal issues related to digital money, many challenges remain, and new digital money services may emerge in the future. It is considered important that examinations from a legal and institutional perspective regarding digital money continue to deepen. We hope that research at the Institute for Monetary and Economic Studies will contribute to future discussions.

This issue was written by Hiromune Kodama and Yuta Ishioka. The content and opinions in this issue are those of the Institute for Monetary and Economic Studies staff and do not represent the official views of the Bank of Japan or the Institute for Monetary and Economic Studies.

Please follow us to read more about Finance & FinTech in Japan, like hundreds of readers do every day. We invite you to also register for our short weekly digest, the “Japan FinTech Observer”, on LinkedIn, or directly here on the platform.

We also provide a daily short-form Japan FinTech Observer news podcast, available via its Podcast Page. Our global Finance & FinTech Podcast, “eXponential Finance” is available through its own LinkedIn newsletter, or via its Podcast Page.

Should you live in Tokyo, or just pass through, please also join our meetup. In any case, our YouTube channel and LinkedIn page are there for you as well.